Employee Equity and ESOPs in Australia: What Founders Should Know Early

If you are building a startup in Australia, at some point you are going to need to figure out equity. Specifically, how to share it with the people helping you build the thing. An employee share option plan (ESOP) is one of the most effective ways to do that. It lets you offer ownership upside to your team without burning through cash you do not have yet. When structured properly, it can be the difference between landing a critical hire and watching them walk to a competitor offering a bigger salary.

But ESOPs are also one of the most misunderstood areas of startup law in Australia. Get it wrong and you risk adverse tax outcomes for your employees, compliance issues, or a plan that does not do what you think it does. This article breaks down the fundamentals.

What is an ESOP, really?

An ESOP is a structured arrangement through which a company grants options or rights over ordinary shares to employees, contractors or directors. The recipient does not get shares straight away. Instead, they receive an option to acquire shares at a predetermined price (the exercise price) at a future point in time, subject to certain conditions being met.

The logic is simple: if the company grows in value, the gap between the exercise price and the eventual market value of the shares is the economic benefit to the option holder. That upside is what makes equity compelling. It aligns your team's financial outcomes directly with the success of the business, and that alignment is powerful.

Key Plan Features to Get Right

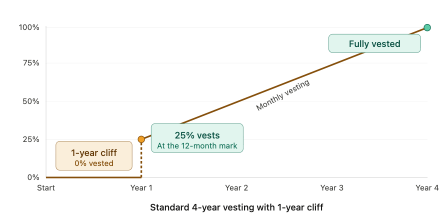

Vesting. The most common structure in the Australian startup ecosystem is a four-year vesting schedule with a one-year cliff. No options vest during the first 12 months. At the one-year mark, 25% of the total grant vests in one hit. The remaining 75% then vests monthly or quarterly over the following three years. The cliff protects the company from giving equity to someone who leaves after a few months.

Leaver provisions. Most plan rules distinguish between a "good leaver" (someone departing in good standing) and a "bad leaver" (someone terminated for cause, such as fraud or serious misconduct). The treatment of vested and unvested options differs depending on which category applies. Founders should make sure these definitions are fair and clearly drafted.

Post-departure exercise window. Some plans require departing employees to exercise their vested options within a short window (say, 90 days) after leaving. If the exercise price has increased substantially since the original grant, this can put a departing employee in a tough spot. Think carefully about whether this clause is necessary. A longer window, or removing the requirement altogether, can be a meaningful signal of fairness.

Tax: The Startup Concession Under Division 83A

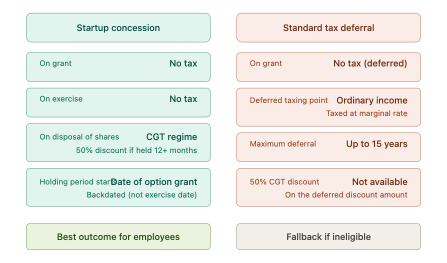

This is where it gets important. The taxation of employee share schemes in Australia is governed by Division 83A of the Income Tax Assessment Act 1997 (Cth). The general rule is that when an employee receives shares or options at a discount to market value, that discount is assessable income. For startup employees holding illiquid equity, that creates a real problem: a tax bill with no cash to pay it.

The ESS startup concession, introduced in 2015, changed this for qualifying companies. Under the concession, the discount is reduced to nil for income tax purposes. No tax on grant. No tax on exercise. The employee is only taxed when they eventually sell the shares, and at that point the disposal falls under the capital gains tax regime. The CGT holding period is also backdated to the date the options were originally acquired, not the date of exercise. So if the employee held options for more than 12 months before selling the resulting shares, they may be entitled to the 50% CGT discount, effectively halving their taxable gain.

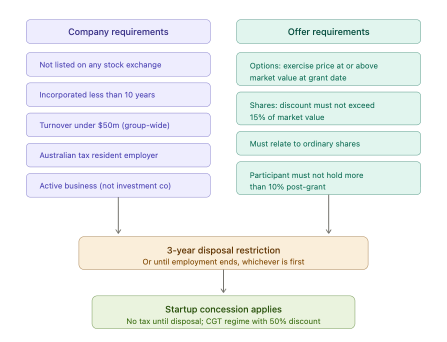

To qualify, the company must meet a number of conditions:

Not listed on any approved stock exchange.

Incorporated for less than 10 years.

Aggregated turnover (including connected entities) of less than $50 million.

An Australian tax resident, operating an active business (not a holding or investment vehicle).

For options: the exercise price must be at or above the market value of shares at the date of grant. For shares: any discount must not exceed 15% of market value.

The participant must not hold more than 10% of shares or voting rights after the grant.

ESS interests must be subject to a genuine three-year disposal restriction (or until employment ends, whichever is first).

Keep in mind that eligibility can change. A company may "age out" once it exceeds the 10-year incorporation threshold or breaches the $50 million turnover cap. Prior qualifying grants are not affected, but future grants will need to be structured under the general ESS tax deferral rules, where the deferred amount is taxed as ordinary income (meaning the 50% CGT discount is not available on that portion).

Corporations Act Compliance

Since 1 October 2022, employee share schemes for unlisted companies are primarily governed by Division 1A of Part 7.12 of the Corporations Act 2001 (Cth). This replaced the old ASIC Class Order framework and significantly simplified the regulatory requirements, providing broad exemptions from financial product disclosure and licensing obligations for qualifying offers. For companies outside these exemptions, alternative pathways exist, including the small-scale offering exemption (up to 20 persons, no more than $2 million in any 12-month period) and the senior manager exemption under section 708(12).

The Bigger Picture: Capital Structure

ESOP equity does not exist in a vacuum. Option pools should always be calculated on a fully diluted basis, accounting for all outstanding shares, options and convertible instruments such as SAFE notes. Founders and employees should also understand how investor preferences affect the economics of their equity. A liquidation preference entitles certain investors to receive their invested capital back before ordinary shareholders see any distribution on exit. Anti-dilution clauses can result in additional shares being issued to investors in down-round scenarios, further diluting the ESOP pool. These are not abstract concepts. They can mean the difference between a meaningful payout and a disappointing one. Be transparent with your team about how these dynamics work.

How Zed Law Can Help

At Zed Law, we advise Australian startups on the design, implementation and ongoing management of ESOPs. We understand both the legal framework and the practical realities of building a company, and we work with founders to structure plans that are compliant, tax-effective and genuinely useful as a talent tool. That includes drafting bespoke plan rules, advising on startup concession eligibility, conducting share capital reviews ahead of fundraising rounds, and reviewing existing plans for ongoing compliance.

If you are thinking about setting up an ESOP or need an existing plan reviewed, get in touch via the booking link or contact form below.

LET'S GET STARTED

Book in with the button below or complete the form and we’ll be in touch.

Disclaimer: This article is intended as general information only and does not constitute legal or tax advice. The information in this article is current as at March 2026. Specific advice should be obtained in relation to your particular circumstances.

© 2026 Zed Law. All rights reserved.